Nielsen Valuation California is your dedicated business valuation partner across the Golden State. We deliver precise, defensible appraisals that are independent, non-speculative, and fully IRS-compliant. Talk with us today about your California business appraisal.

Our Locations

Nielsen Valuation California has a local presence in the following locations:

We also conduct on-site interviews statewide, including Sacramento, San Jose, Fresno, Bakersfield, Long Beach, Riverside, Santa Ana/Irvine, Ventura, Santa Rosa, and throughout the Inland Empire and Central Valley.

Nielsen Valuation California in Brief

Nielsen Valuation California provides thorough, judgment-driven, and truly independent assessments of private companies.

Our work focuses on fair market value and resists speculation. We anchor conclusions in what the business demonstrates today and what was reasonably knowable on the valuation date.

To get there, we study the company in depth and normalize income statements and balance sheets to remove non-recurring items, related-party noise, and accounting distortions before any math begins.

When discounts for lack of marketability are warranted, we support them with observable market behavior and transaction evidence. Not abstract theory.

The outcome is a credible valuation that stands up to scrutiny. Useful for sales, acquisitions, shareholder matters, divorce, litigation, buy-ins/buyouts, and strategic planning.

IRS-Compliant Business Valuations

We follow the guidance of IRS Revenue Ruling 59-60 and align our work with how real buyers and sellers make decisions.

That means we give substantial weight to real-world transactions and risk—not just to checklists from ASA, NACVA, or AICPA, so your valuation reflects the marketplace, not a template.

In practice, here’s what we avoid:

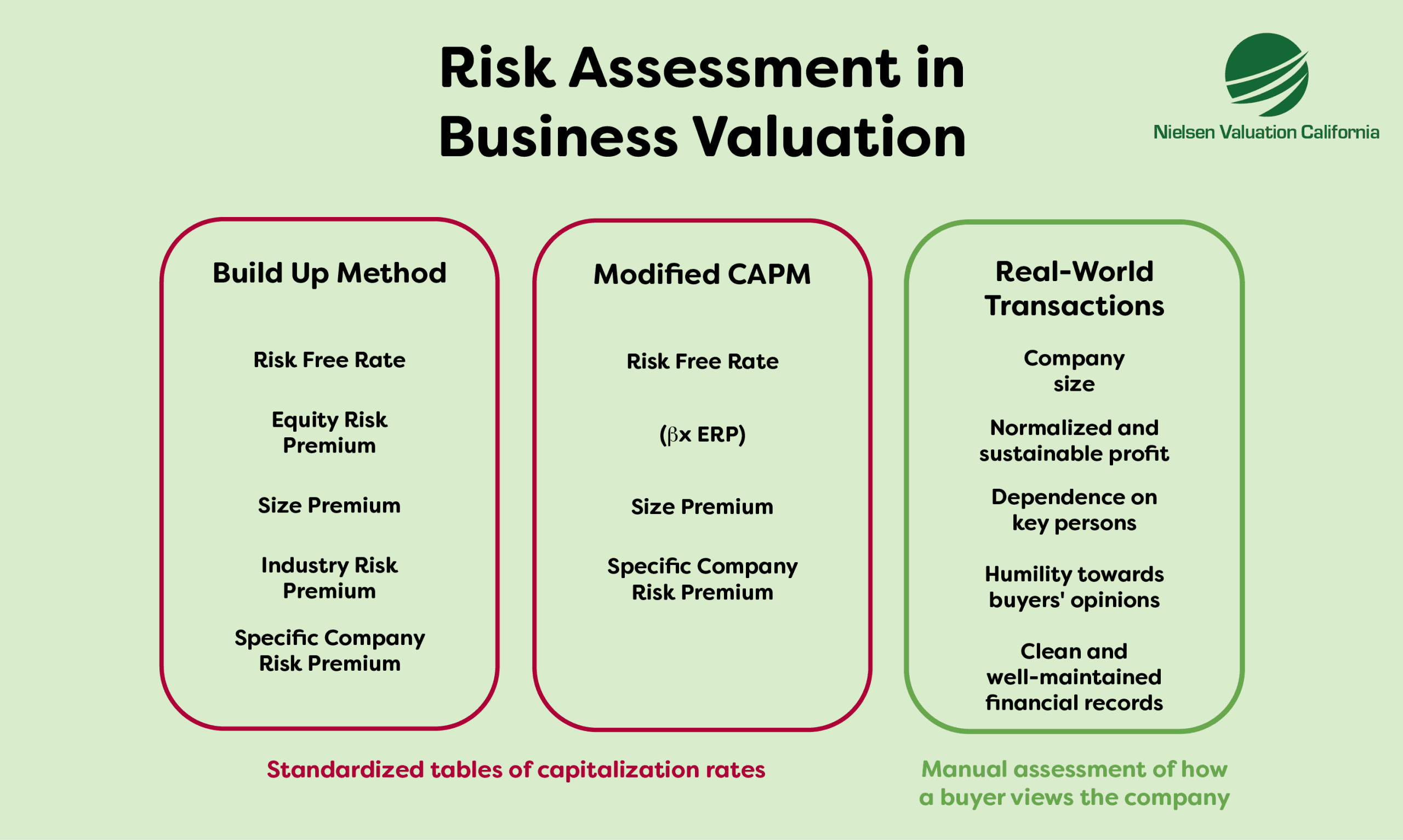

We Don’t Lean on Cap-Rate Tables

We never default to standardized capitalization-rate tables in our California business valuations. They’re convenient, but rarely capture a specific company’s risk profile, earnings consistency, and operational reality.

Instead, we evaluate business model, volatility, customer concentration, depth of management, and more to derive a rate that fits the subject company.

This is consistent with IRS 59-60, which notes:

”No standard tables of capitalization rates applicable to closely held corporations can be formulated.”

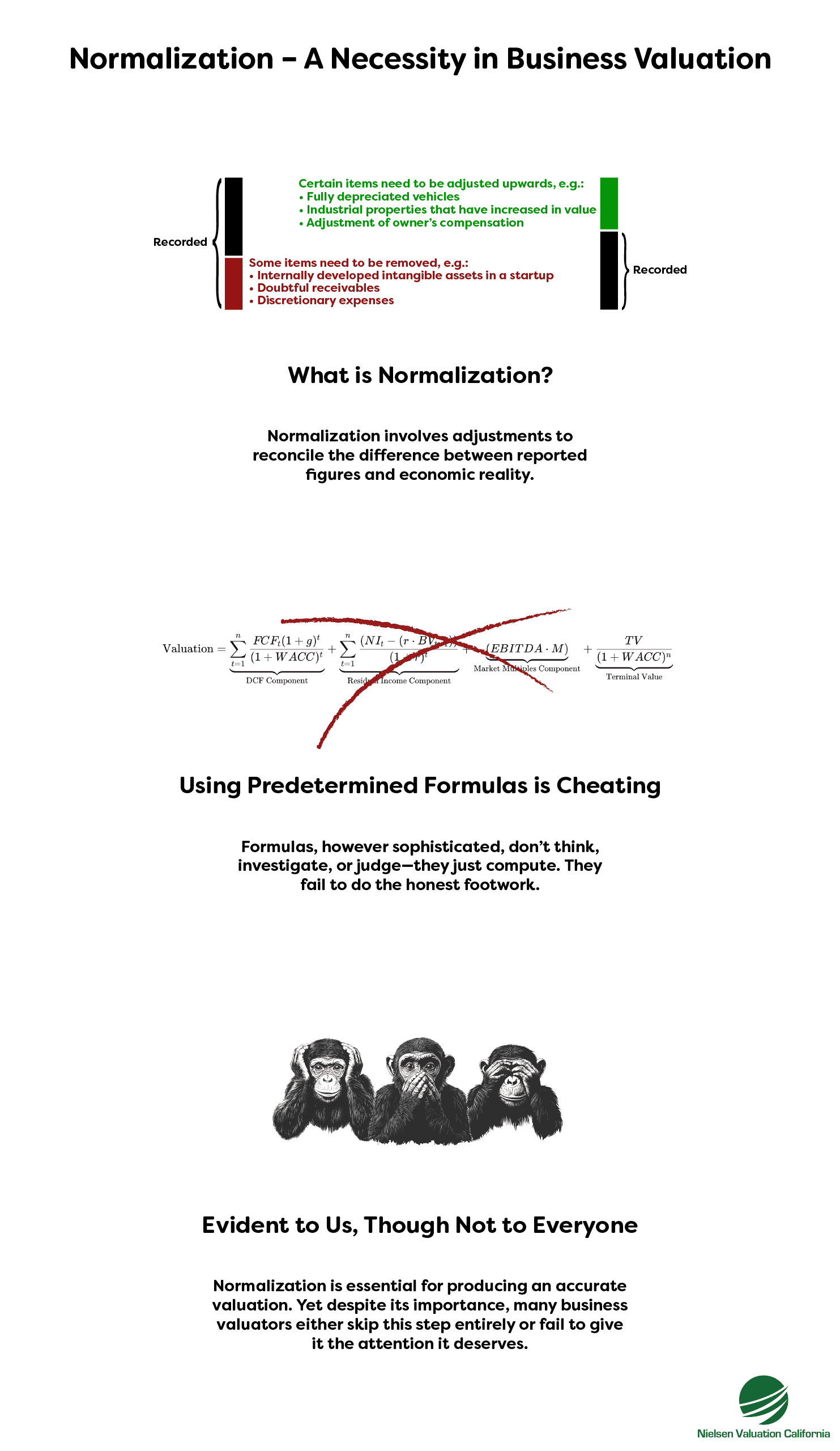

We Don’t Use One-Size-Fits-All Formulas

Formulaic “valuations” that simply plug financials into a template ignore context, and misprice companies.

Our process is the opposite: company-specific analysis backed by interviews, document review, and when appropriate, a site visit.

The IRS is explicit:

“Valuations cannot be made on the basis of a prescribed formula.”

“No general formula may be given that is applicable to the many different valuation situations arising in the valuation”

“Such a process excludes active consideration of other pertinent factors, and the end result cannot be supported by a realistic application of the significant facts in the case except by mere chance.”

Every engagement is bespoke. We study operating history, earnings quality, and prospects—then apply methods that fit the assignment.

We Don’t Assume Theoretical Marketability Discounts

Marketability discounts should reflect how interests actually trade. Nielsen Valuation California supports any discounts with observed transaction behavior and market dynamics, not abstract studies.

The contents of RR 59-60 are available in the appendix of this document.

Our Business Valuation Services in California

Your Independent California Business Valuation

From family-owned companies to lower-middle-market firms, we deliver independent valuations across California. Our single goal: determine true fair market value so you can act with confidence. (We don’t value start-ups.)

Selling a Business

Heading to market? A credible, independent valuation helps set a defensible asking price, attracts qualified buyers, and speeds negotiations.

Exit Planning

Plan ahead to maximize proceeds. We identify the value drivers and value detractors so you can shore up financials, systems, and contracts before buyers start diligence.

Investments

Considering an acquisition in California? We serve as an independent voice—screening opportunities, supporting negotiations, and verifying whether the price fits the facts.

Mergers & Acquisitions

Enter negotiations with confidence. Nielsen Valuation California provides independent, court-tested valuations that strengthen your position and build trust with counterparties and lenders.

Small Business Valuation

We specialize in closely held companies. If it’s a private business (non-startup), we can value it. Efficiently and objectively.

Business Appraisals for Financial Planning

With a clear, unbiased valuation, you can make smarter decisions around succession, capital allocation, and long-term strategy.

ESOPs

Nielsen Valuation California determines supportable share prices for ESOP transactions and annual updates.

Partnership Buyouts

Need a fair price for a partner buy-in or buyout? Our neutral valuation helps align expectations and smooth the agreement process.

Shareholder Agreements & Disputes

Prevent or resolve disputes with a well-supported opinion of value for buy-sell agreements, capital raises, and minority interest matters.

Business Valuation in Divorce

When equity is part of a marital estate, our objective valuation helps both sides move forward with clarity.

Litigation

Nielsen Valuation California has deep expert testimony and litigation support experience. Our valuations adhere to IRS guidance and withstand courtroom scrutiny.

Estate Planning

Plan gifts, trusts, and estates with a well-documented opinion of value that aligns with IRS expectations.

Business Valuation for Tax Purposes

Transactions and filings demand accuracy. We help you get the numbers right—before they go to the IRS or state authorities.

How To Value a Business – Business Valuation Methods

Picking the right valuation method, and applying it correctly, is essential to fair market value.

When you engage us, we select methods that fit the company’s economics and the purpose of the assignment, then apply them with rigor.

Most techniques roll up into three families:

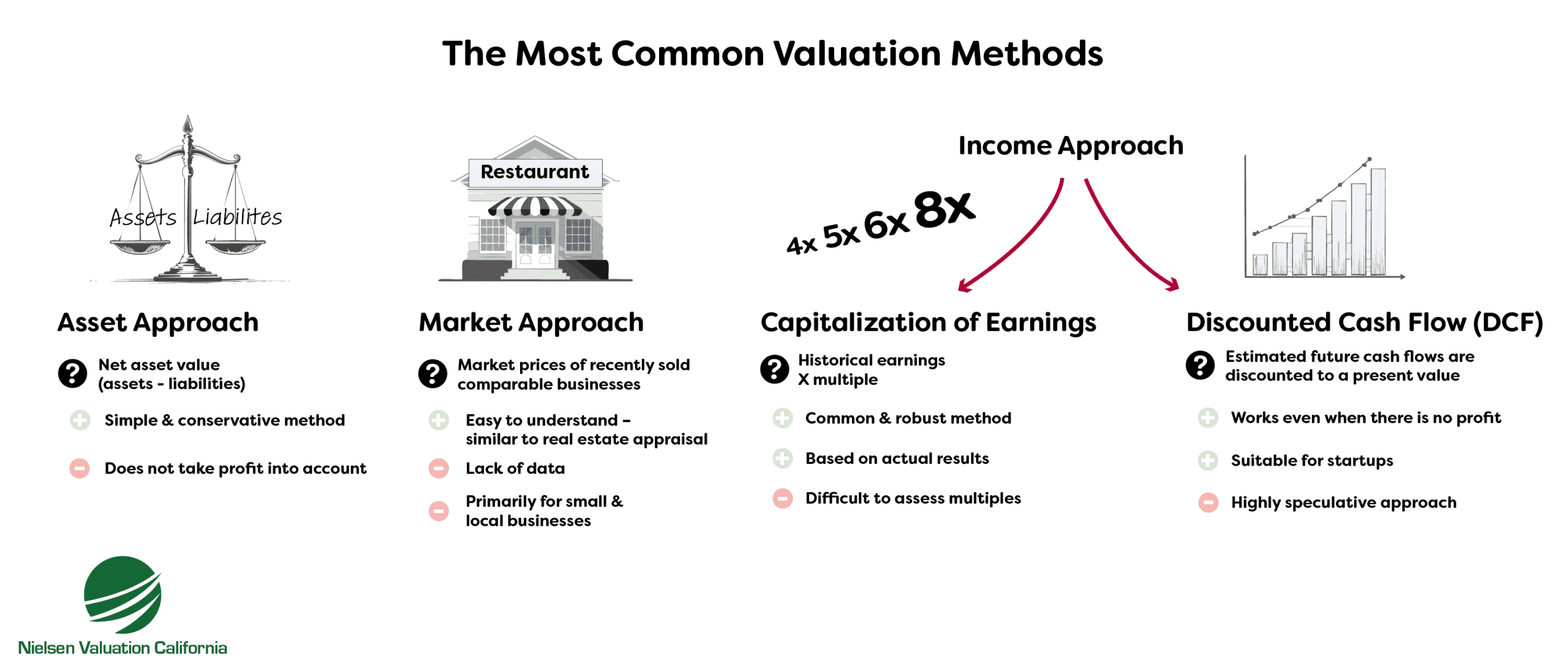

- Asset Approach

- Income Approach

- Market Approach

Here’s a quick tour:

Asset Approach

The asset approach estimates value by determining net asset value at market—assets minus liabilities, adjusted to what they’re worth today (not just book value).

It’s powerful for asset-intensive companies and in wind-down scenarios. Because it ignores earnings power, we often pair it with the income approach.

Read more about the asset approach

Market Approach

The market approach looks to what comparable businesses sell for and applies those multiples to the subject company.

Its strength is reality: it’s grounded in actual deals. Accuracy depends on cleaning outliers and using reliable, well-documented data.

We frequently combine it with the income approach to triangulate fair market value.

Read more about the market approach

Income Approach

The income approach ties value to risk and expected future earnings, commonly via capitalization of earnings or, when appropriate, discounted cash flow (DCF).

Read more about the income approach

Combining & Weighting Methods

It’s common to combine or weight approaches. The key is judgment—never a mechanical formula. IRS 59-60 cautions against averaging factors without context.

For example (illustrative only):

- Assets of $1,000,000 and liabilities of $500,000 suggest a $500,000 net asset value.

- Earnings of $3,000,000 and a justified multiple of 3 imply $9,000,000 via the income approach.

- Weighting the two at 50/50 would yield $4,750,000—but only if that weighting reflects the company’s facts, not a rule of thumb.

As the IRS notes, arbitrary weighting “serves no useful purpose.” Sound valuations apply expert judgment to the data at hand.

Normalization Is Critical

Before any calculation, normalize the financials. The math is easy; knowing which inputs are faithful to economic reality is the hard part.

We remove unusual gains/losses, related-party items, and accounting distortions so the valuation reflects true earning power and market-level asset values.

Common inflations:

- Intercompany receivables unlikely to be collected

- Internally developed intangibles capitalized above market

- Under-market owner wages inflating EBITDA

Common deflations:

- Real estate carried at decades-old cost instead of current value

- Non-operating or discretionary expenses depressing earnings

- Fully depreciated but productive equipment understated on the balance sheet

Whether applying income or asset methods, normalization is non-negotiable. Quality comes from disciplined analysis, not padding a report.

How Much Is My Business Worth?

When you price a business for sale, aim for fair market value—the price at which an informed, willing buyer and seller would transact without compulsion. The IRS defines it as:

“Define fair market value, in effect, as the price at which the property would change hands between a willing buyer and a willing seller when the former is not under any compulsion to buy and the latter is not under any compulsion to sell, both parties having reasonable knowledge of relevant facts. Court decisions frequently state in addition that the hypothetical buyer and seller are assumed to be able, as well as willing, to trade and to be well informed”

Historical results matter. The IRS cautions against mechanical five- or ten-year averages that ignore current trends and prospects:

“Prior earnings records usually are the most reliable guide as to the future expectancy, but resort to arbitrary five-or-ten-year averages without regard to current trends or future prospects will not produce a realistic valuation.”

Two misconceptions often inflate seller expectations:

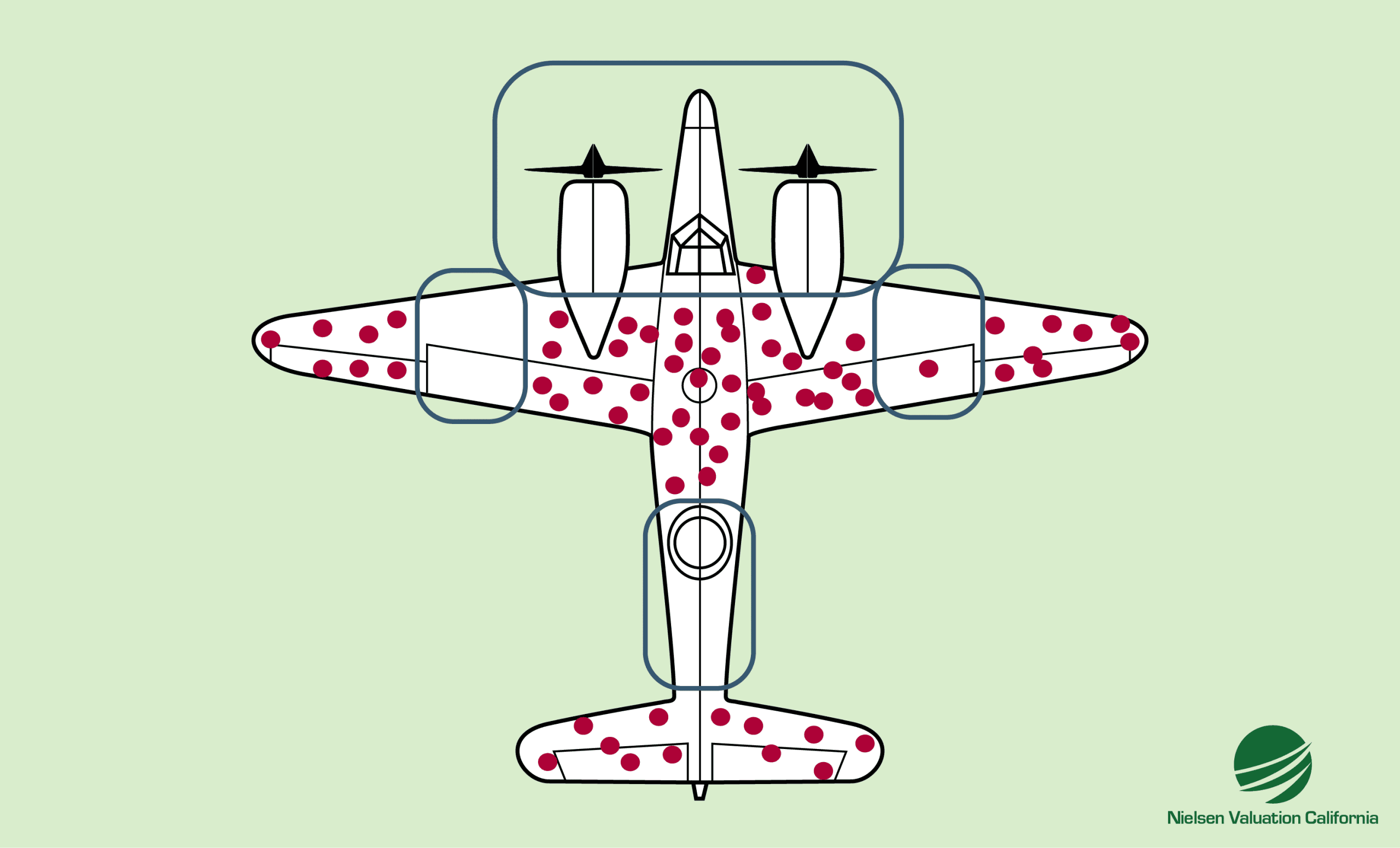

Common Mistake #1: Survivorship Bias

During the Second World War, analysts mapped the bullet holes on aircraft that managed to return to base. The early takeaway was to reinforce the spots that showed the most damage.

That conclusion missed a critical point. Few of the surviving planes showed hits to the cockpit, engines, or certain wing sections—not because those areas were safe, but because aircraft struck there didn’t make it home. The missing data lived with the planes that crashed.

This is the classic trap of survivorship bias, and it shows up everywhere in business.

Entrepreneurs often benchmark against headline winners—think Spotify, PayPal, Microsoft, Meta, or Alphabet—when gauging their own odds. But those companies are the visible exceptions. For every standout, many more ventures never reach the spotlight.

Base rates are sobering: roughly one in ten startups endures over the long haul. The rest shut down, with about a tenth of all startups failing in their first year.

Because of this skewed reality, buyers tend to price in risk and uncertainty, while sellers, influenced by success stories, anchor to higher expectations. The gap between those perspectives often leads to lower offers than owners anticipate.

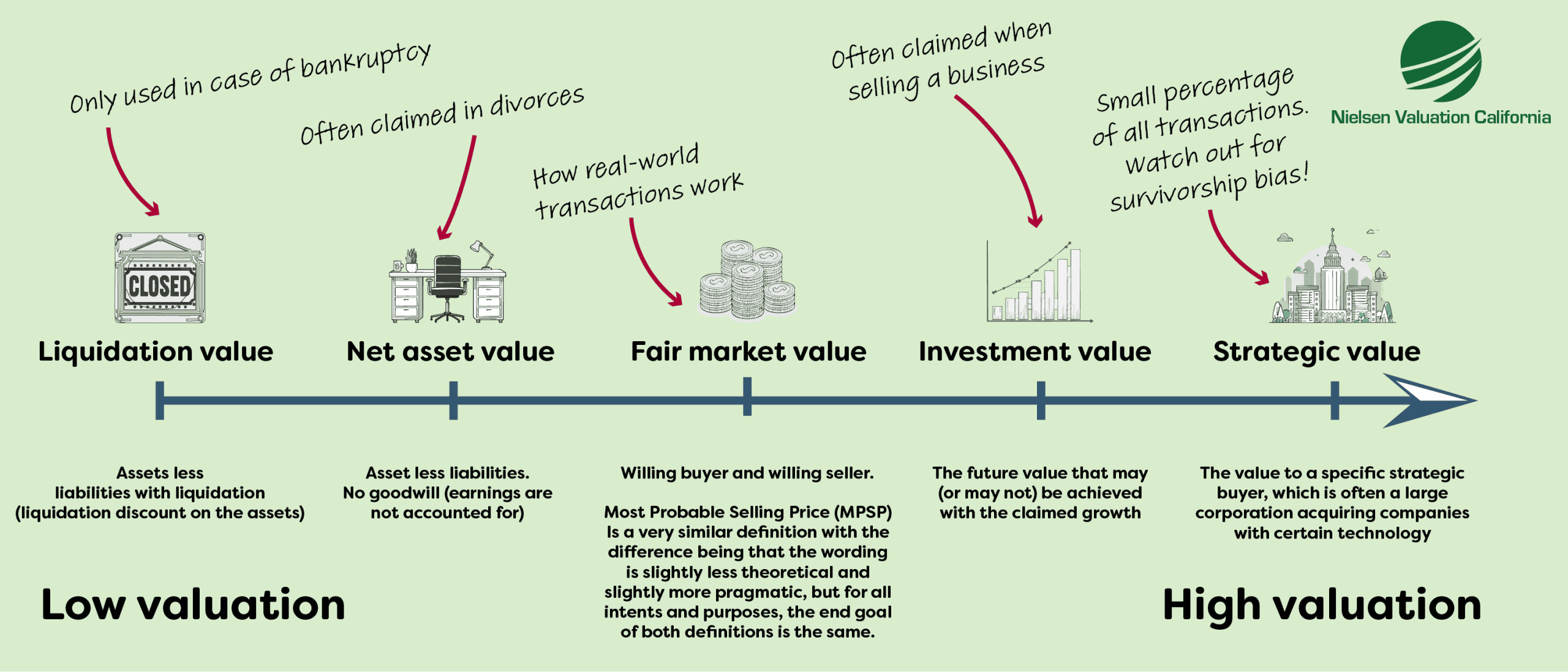

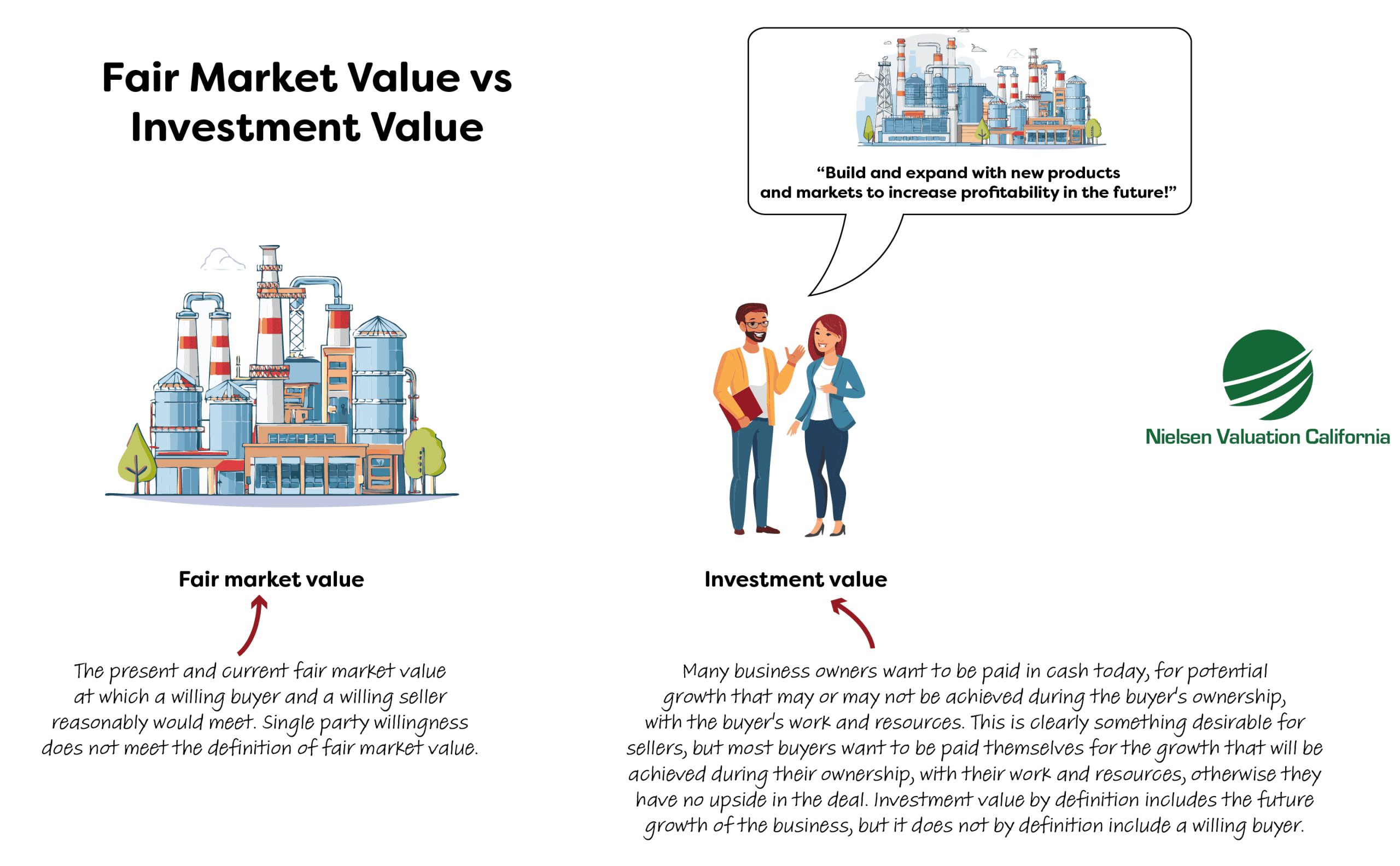

Common Mistake #2: Mixing Fair Market Value with Investment Value

Sellers sometimes want today’s cash price to reflect tomorrow’s potential: growth that the buyer must fund and execute. Buyers, however, expect to earn that upside themselves.

Investment value (what it’s worth to you) can exceed fair market value (what the market will pay). Buyers typically pay fair market value.

Selling Potential vs. Selling Reality

“Pay us for what this business could become.” That pitch conflicts with 59-60, which centers on facts known or knowable on the valuation date. Price what’s being transferred today—not a hypothetical future version.

The yacht analogy holds: you don’t price a dinghy like a super-yacht because it might get upgrades someday. Same for businesses.

Conclusions Must Match Facts on the Valuation Date

Per 59-60, conclusions must reflect the facts as they exist at the time. Just as rational market participants would price them. That’s the standard we apply.

Our opinions are grounded in evidence, not wishful thinking, producing actionable, defensible valuations.

7 Common Business Valuation Mistakes

- Method mismatch: Using only an income method for thin or volatile earnings, or only an asset method for a high-growth service firm, skews value.

- Skipping normalization: Book values and raw EBITDA are rarely “clean.” Without market adjustments and add-backs, outputs mislead.

- Flat-averaging earnings: Small businesses swing year to year. Treating each period as equally representative ignores what buyers scrutinize most: why a given year is (or isn’t) indicative.

- Valuing numbers, not businesses: Behind the spreadsheet are customers, contracts, key people, and processes. Miss the story and you’ll miss the value.

- Calculator valuations: Pre-set formulas can’t replace analysis. Wrong inputs in, wrong number out—no matter how sleek the tool.

- Treating the value as absolute: Two qualified appraisers can disagree. Markets decide. Aim for reasonable, supportable conclusions, not wishful ones.

- Relying solely on a broker’s price: Commissions can bias pricing upward. A neutral valuation increases the odds of an actual closing.

Why Choose Nielsen Valuation California?

Nielsen Valuation California is a trusted, independent partner for business owners, attorneys, and advisors statewide.

We accept no sales commissions and no success fees. Our only agenda is to deliver a balanced, well-supported opinion of value.

Built for court and the real world: our methodology aligns with IRS guidance and actual transaction behavior. We avoid speculation and rely on evidence.

We normalize financials to reflect economic reality and apply market-grounded discounts only when warranted.

Every assignment is tailored to the company and purpose. When helpful, we visit the site and interview stakeholders.

Our reports are concise, plain-English, and built to withstand scrutiny. They’ve been used successfully in court.

If you need a dependable business valuation in California—for a sale, acquisition, dispute, divorce, tax, or planning matter—we’re ready to help.

Request a Business Valuation in California

Let’s discuss your goals and timeline. Contact us for a free consultation and quote.